Miners power the transaction and verification processes that make most virtual currencies function. As a result, mining has a dominant position in the ever-expanding world of virtual currency.

Ever since the bitcoin genesis block, coin mining has been the lynchpin of the cryptocurrency ecosystem.

For many, cryptocurrency mining has grown into a thriving business characterized by substantial investments in complex systems and costly resources. As cryptocurrency mining becomes more costly and competitive, miners are looking to take greater advantage of tax breaks to help them maximize their profits.

Taxable income

The Internal Revenue Service treats cryptocurrency mining income as business income, even for miners who only operate on a small scale. Anyone who receives mining rewards worth over $400 in a calendar year must report their activity to the IRS.

Miners must report income from every coin they receive in a given tax year, at the market value of the coin at the time it is received. Those who own their mining equipment individually must report their mining income as self-employment income on Schedule C of their tax return. The net income on a Schedule C is subject to ordinary income tax plus a 15.3 percent self employment tax.

From a tax perspective, however, some coin miners prefer to own their mining equipment through a company and be treated as business entities rather than as self-employed individuals. Corporate tax policies can be more generous than individual tax rules if there is significant net income for the mining business.

If the net income exceeds $60,000, for example, an S Corporation (or a LLC taxed as an S Corp) may make sense. Utilizing an S Corporation, you may be able to eliminate paying the 15.3 percent self employment tax charged to individuals on a portion of the mining income.

In a high-cost industry like cryptocurrency mining, these tax benefits can carry substantial value. However, depending on the state in which a company is registered and does business, business entities other than an S Corporation may make more sense. is a lifelong entrepreneur and Crypto and Taxes 2018 series.

Be sure to consult a credentialed tax professional to discuss the best options for your particular scenario. Business entities also generally have a lower instance of audits than self-employed Schedule C filers.

Expenses and losses

Good mining operations can be incredibly profitable. However, cryptocurrency mining is full of technical and financial pitfalls that can send a mining business into the red.

The most significant cost facing just about any cryptocurrency mining operation is the hardware and electricity used to keep it going. Miners living in areas with deregulated electricity marketplaces are advised to rate shop to pursue cheap rates. A few cents per kilowatt-hour can mean the difference between profit and loss.

Miners with access to cheap electricity do brandish this substantial competitive edge in regards to profitability. Even mining businesses in higher cost areas that aren’t so lucky can still deduct their mining-related electrical costs from their business income, reducing their net profit. For miners that spend thousands of dollars each year purchasing electricity, this tax deduction can quickly add up to a substantial value.

Cryptocurrency mining uses a staggering amount of electricity, and all that power goes towards running complex mining hardware systems called «rigs.» A mining rig includes various pieces of specialized equipment, including graphics cards and a GPU, a microprocessor specialized for graphics calculations.

Better hardware specs can be very expensive, but they lay the groundwork for the efficiency of your mining operation. As a result, efficient rigs often require coin miners to lay out some serious cash.

Fortunately, however, the IRS allows miners to deduct the depreciation of their mining equipment. Using the Accelerated Cost Recovery depreciation methods recognized by the IRS, coin miners typically deduct the value of their rigs over a span of three to five years. However, in most cases a deduction of the entire purchase price of equipment in the year it was purchased can be made using special Section 179 depreciation rules.

Some rigs are simply not powerful enough to generate a profit, particularly for coins that a particularly difficult to mine. After adding up the cost of electricity, office space, hardware and other mining expenses at the end of the year, some miners discover that they actually lost money in their operations.

If there is a net loss on a mining operation, those losses can be used to offset other income. Mining companies should accurately document all business expenditures that are related to the endeavor so they are prepared to maximize the tax savings.

A business and an investment

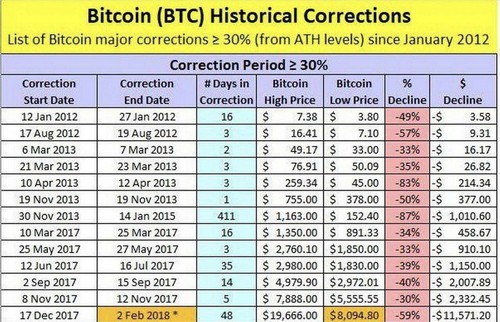

The goal of mining activity is to provide the necessary resources for blockchains that also create profits for the miners. This profit oftentimes hinges on the market value of the cryptocurrency being mined. A bad day in the cryptocurrency market can mean the difference between profit and loss, so talented coin miners must be both competent technicians and skilled investors.

Typically, cryptocurrency miners focus their resources on coins that return good value. Because some crypto coins offer higher rewards for miners than others, mining operations sometimes swap their mined cryptocurrency to another crypto that they prefer to hold on to. When miners make this exchange one coin for another, they are actually selling the first coin in return for buying the second coin which in turn creates a capital transaction.

These coin-for-coin swaps are required to be reported separately and additionally to the actual mining income as business income. They create short- or long-term capital gains or capital losses to be included on Form 8949 which then flows to Schedule D.

Long-term capital gains are taxed at favorable rates and are applicable to those coins held on to for over one year. Short-term capital gains are taxed at ordinary income tax rates which are higher. There are numerous accounting methods potentially available to apply to these capital gain transactions to create tax efficiency when reporting the subsequent sales of any mined coins.

Audit safety

Safety is critical to success.

Coin mining income received individually is usually taxed as sole proprietorships on a Schedule C which are audited much more frequently than individuals without self-employment income.

As a result, coin miners should always make sure to keep their financial records in order in case of an audit.

From the classification of mining income to deductions, depreciation schedules for rig equipment to having a second reporting and tax requirement after the mined coins are sold, tax rules for cryptocurrency miners can get complicated.

Anyone who generates more than a few hundred dollars per year in cryptocurrency mining income would be wise to speak with a credentialed tax professional – either a certified public accountant, a tax attorney or an enrolled agent.